Shutterstock

Venture Deals in LA Are Slowing Down, And Other Takeaways From Our Quarterly VC Survey

It looks like venture deals are stagnating in Los Angeles.

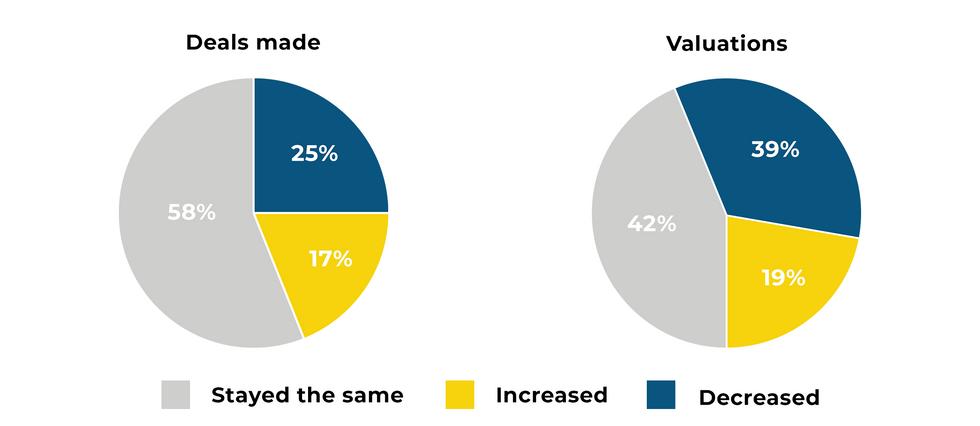

That’s according to dot.LA’s most recent quarterly VC sentiment survey, in which we asked L.A.-based venture capitalists for their take on the current state of the market. This time, roughly 83% of respondents reported that the number of deals they made in L.A. either stayed the same or declined in the first quarter of 2022 (58% said they stayed the same compared to the fourth quarter of 2021, while 25% said they decreased).

That’s not hugely surprising given the sluggish dynamics gripping the venture capital world at large these days, due to macroeconomic factors including the ongoing stock market correction, inflation and Russia’s invasion of Ukraine. While startups and VC investors haven’t been hit as hard as public companies, it looks like the ripple effects are beginning to bleed into the private capital markets.

Image courtesy of Hagan Blount

Image courtesy of Hagan Blount

In addition to slowing deal volumes, most investors said they’re seeing startup valuations lose momentum, as well: Roughly 81% said valuations either stayed the same or decreased from the previous quarter, with nearly 39% noting a decline.

Should that sentiment continue moving forward, it could spell bad news for startups as far as raising the money they need for growth, investors said.

“If I was a startup right now, I would be making sure I have plenty of runway,” said Krisztina ‘Z’ Holly, a venture partner at Good Growth Capital. “When it looks like there's some potential challenges ahead in the market, it’s good to fill your war chest.”

Among VC respondents, about 86% said they believed that valuations in the first quarter were too high—one potential reason why deals slowed down in the first quarter, according to TenOneTen Ventures partner Minnie Ingersoll. She noted that L.A.’s growing startup scene features more early-stage ventures, whose valuations haven’t come down the way later-stage startup valuations have.

“I would say we are just more cautious about taking meetings where the valuations are at pre-correction levels,” Ingersoll said. “We didn’t take meetings because their valuations weren’t in line with where we thought the market was.”

While most respondents said the Russia-Ukraine war didn’t have much impact on their investment strategies, some 22% said it did have an effect—with one VC noting they had to pass on a deal in Russia that they liked.

Is There a Flight Out of Los Angeles?

Los Angeles was heralded as the third-largest startup ecosystem in the U.S. at the beginning of the year, behind only San Francisco and New York. Yet nearly one-third (31%) of VC respondents said that at least one of their portfolio companies had left L.A. within the past year. It won’t come as a huge surprise that the city of Austin, Texas has been one of the prime beneficiaries of this shift—with roughly half of those who reported that a portfolio company had left L.A. identifying Austin as the destination.

The tech industry’s much-hyped “exodus” from California has been widely reported on, especially as more companies have embraced the work-from-home lifestyle and also opted to move their operations to lower-cost cities and states. Most notably, Elon Musk has recently moved two of his companies, electric automaker Tesla and tunnel infrastructure startup The Boring Company, from California to Texas (with both of those firms moving in and around Austin).

“In today's competitive market with lots of capital to invest, we think the next generation of successful VCs are going to be diverse in markets (not just Silicon Valley)... [and] have access to undiscovered founders from everywhere,” said one survey respondent.

NFTs Aren’t Popular With VCs—But Web 3 Is

“It’s the future,” according to one respondent. “Buckle up and get on board.”

Are NFTs...

More than 71% of VC survey respondents said they were bullish on Web3—the new blockchain-enabled iteration of the internet, which promises decentralization and a whole range of applications involving cryptocurrencies, NFTs, DeFi and more. It’s the same sentiment informing Santa Monica-based VC firm M13’s new $400 million fund, which considers Web3 a core piece of its investment thesis.

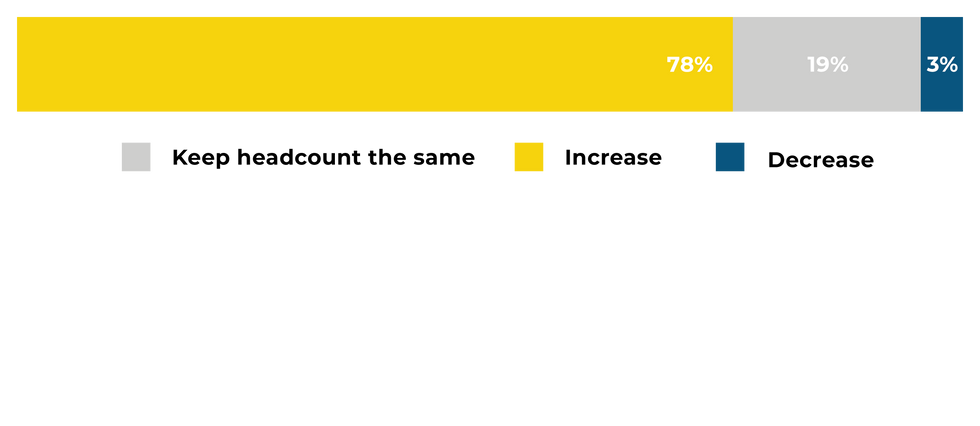

In Q2 2022, do you expect your portfolio companies to:

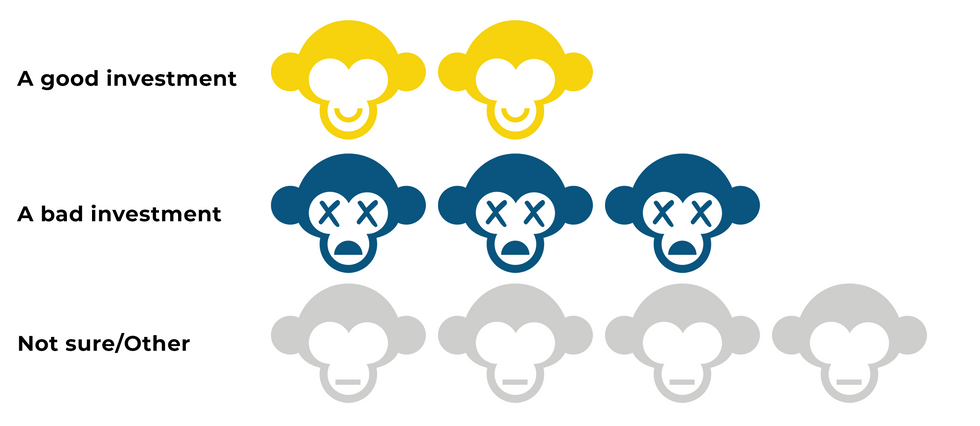

L.A. is home to an ever-growing cadre of Web3-focused startups operating across the realms of finance, entertainment and other industries. But while local investors are willing to pour money into blockchain-related ventures, one segment of the space continues to evoke skepticism: Only 18% of respondents would describe NFTs as “a good investment,” while 33% thought they were “bad” investments and 39% said they were unsure.

As in our last survey several months ago, it appears that NFTs continue to divide opinion, with respondents expressing differing perspectives on their value and utility. One referred to them as “get rich quick schemes,” but added that the art pieces and social communities that emerge from them may be valuable. Another said that “NFTs as a digital medium are a legitimate thing”—but noted the vast majority are “awful investments with no intrinsic value.”

Graphics courtesy of Hagan Blount.

From Your Site Articles

- Los Angeles Venture Funds Grow, but Spend Less in LA - dot.LA ›

- LA's Top Venture Capitalists of 2022 - dot.LA ›

- Los Angeles Venture Capital News - dot.LA ›

- Here Are Los Angeles' Top Venture Capitalists - dot.LA ›

- Venture Deals Fall in LA Amid Economic Worries - dot.LA ›

Related Articles Around the Web

So it felt fitting that Tinder chose the El Rey Theatre in Los Angeles, a venue known for reinvention, to make its case that the category is far from over.

Walking into the El Rey, it was clear Tinder wanted this to feel less like a tech launch and more like a cultural moment. Music was bumping, the room buzzed with chatter and excited energy, red light beams cut through the room, and chandeliers glowed overhead.

At Tinder Sparks 2026: Start Something New, Match Group and Tinder CEO Spencer Rascoff took the stage to outline what the company calls the biggest evolution of the app in years. Tinder remains the largest dating app in the world, used by tens of millions of people across more than 185 countries and responsible for billions of matches every year.

Match Group and Tinder CEO Spencer Rascoff

Match Group and Tinder CEO Spencer Rascoff

Rascoff framed the shift around a broader cultural reality. In a world where people increasingly interact with machines, technology and AI, the need for real human connection has not gone away. If anything, Tinder believes it has only grown stronger.

To respond to that shift, Tinder says it’s focusing on what it calls “sparks,” the moments when a match actually turns into a real conversation.

As Rascoff put it on stage:

“We are not optimizing for swipes or likes. We are optimizing for sparks.”

That philosophy is shaping a wave of new features discussed throughout the keynote by Tinder’s leadership team, including Mark Kantor, SVP and Head of Product, Yoel Roth, SVP of Trust & Safety, and product leaders Claire Watanabe and Hillary Paine.

Image Source: Tinder

Image Source: Tinder

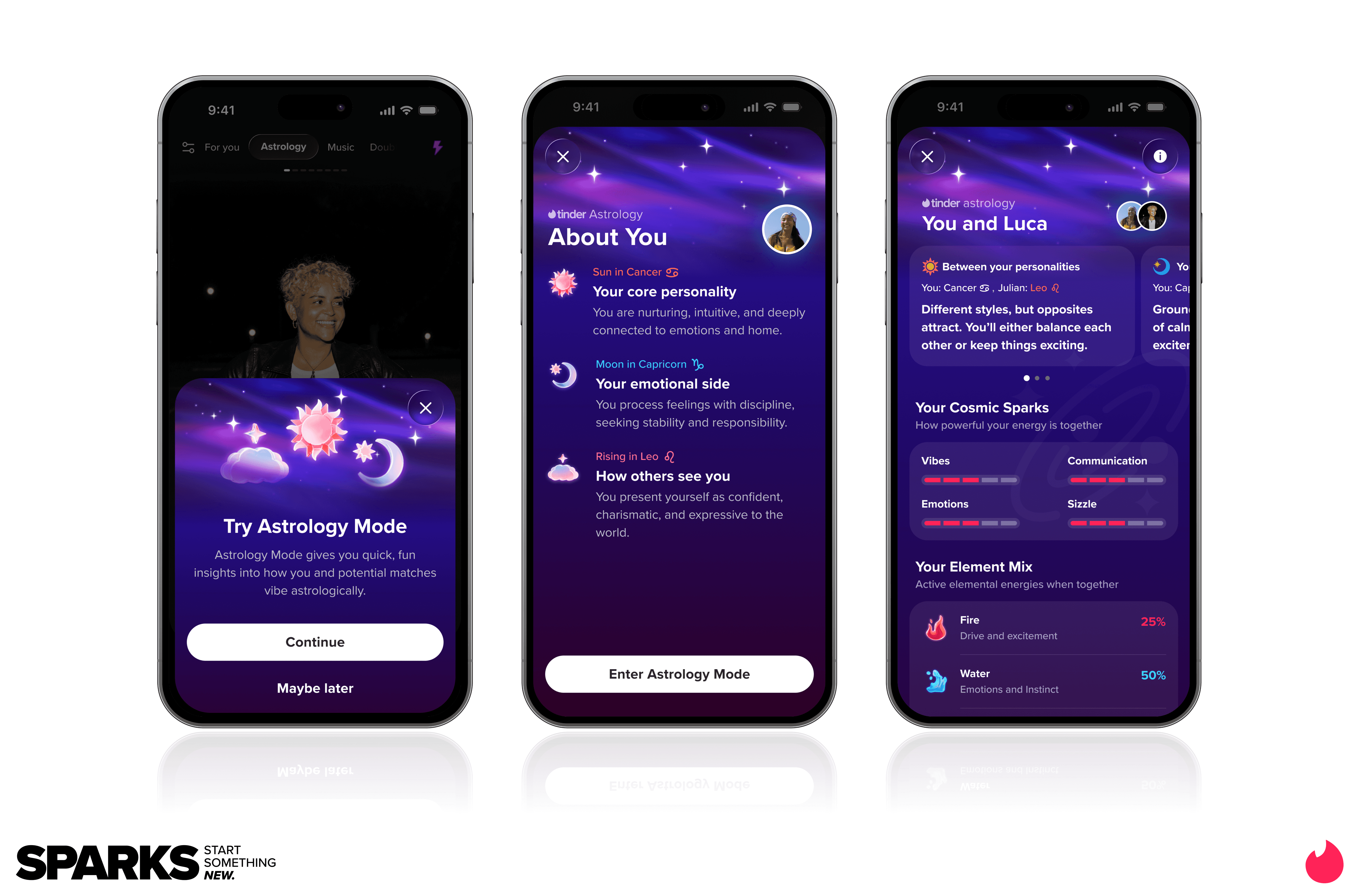

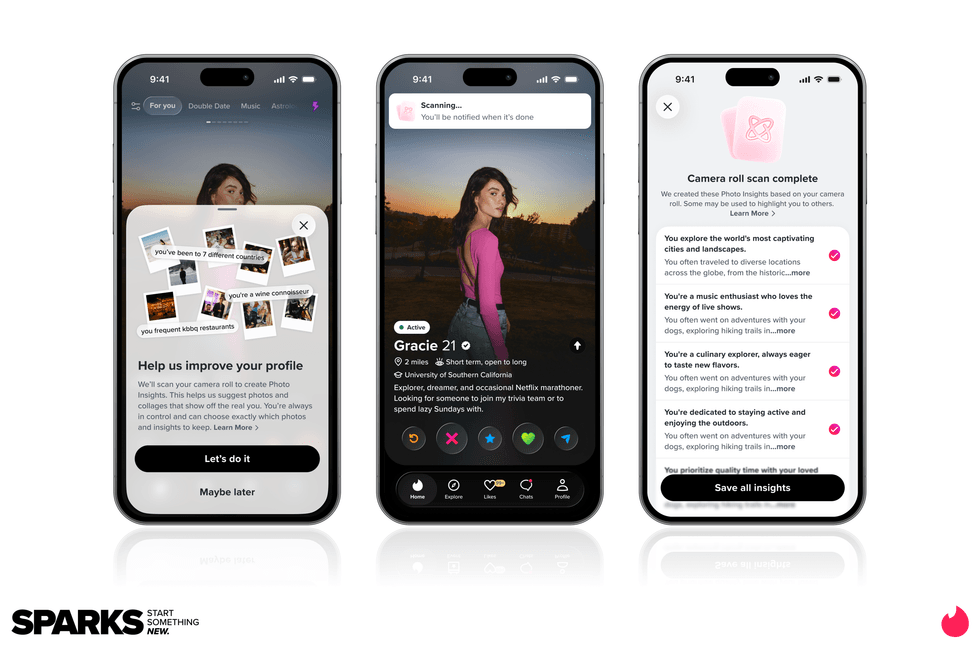

Among the updates are Music Mode, which lets users connect through shared songs and artists, and a new Astrology Mode that highlights compatibility between zodiac signs. Tinder is also leaning further into social dating with Double Date, a feature that lets friends match with other pairs together. The feature is already gaining traction with Gen Z users, reflecting a broader shift toward more social and lower-pressure ways to meet people.

Image Source: Tinder

Image Source: Tinder

Tinder is also redesigning profiles to help users express more personality. New tools can surface stronger photos from a user’s camera roll, improve lighting, and highlight interests more visually, while integrations with platforms like Spotify, Duolingo and the restaurant app Belly bring more of a person’s real life into their profile.

Image Source: Tinder

Image Source: Tinder

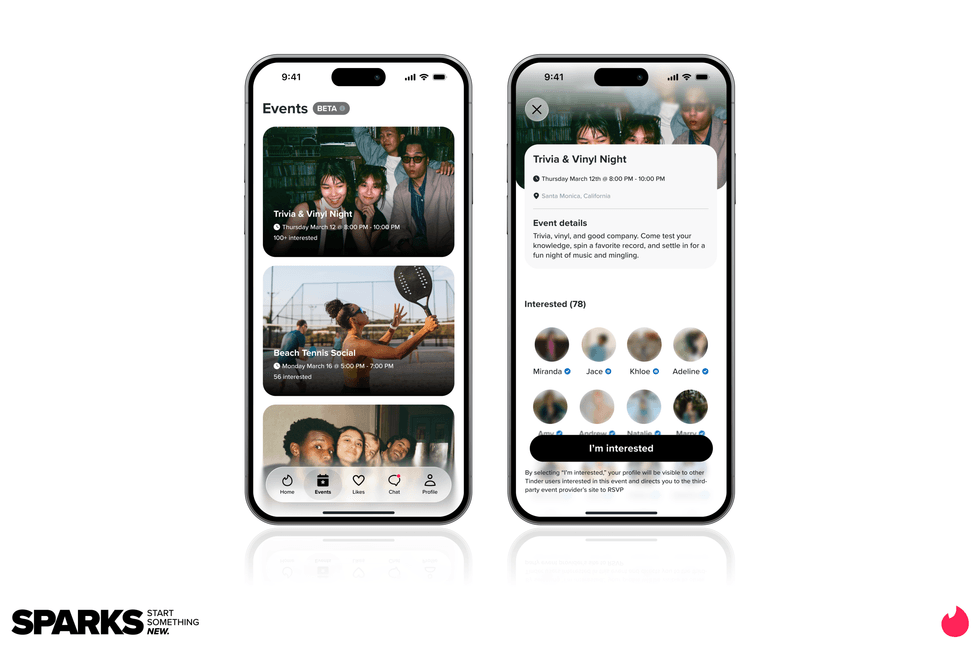

But the most interesting experiment might be happening right here in LA. Tinder is launching IRL Events in the city, letting users browse and RSVP to real-world meetups directly through the app. Think coffee shop raves, trivia nights and pickleball tournaments. The idea is simple. Dating works better when it feels like a social activity instead of an interview.

Image Source: Tinder

Image Source: Tinder

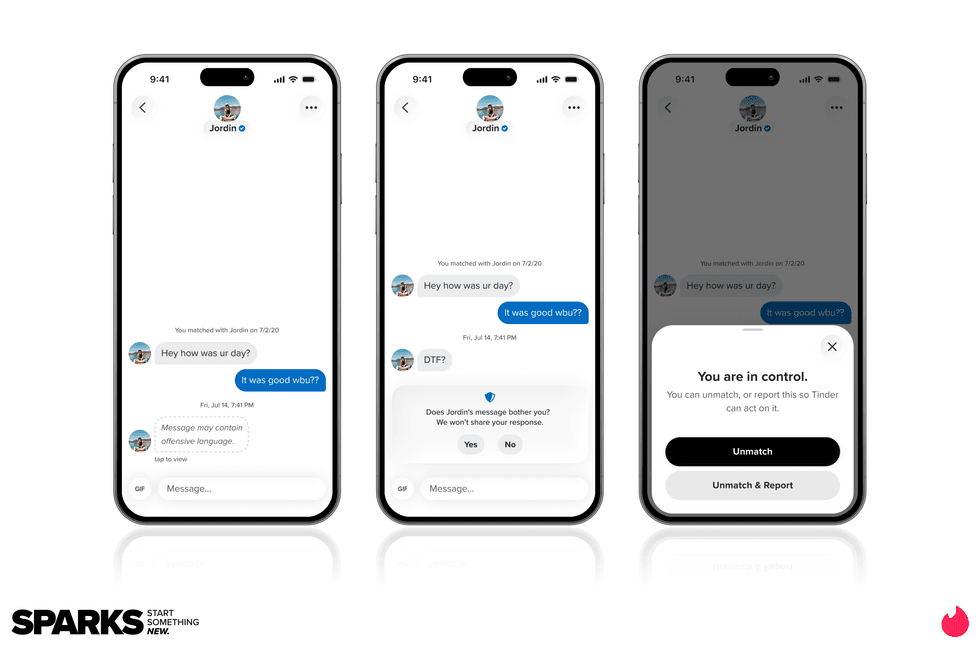

Under the hood, Tinder is also leaning more heavily on AI to improve recommendations. New tools like Learning Mode and Chemistry aim to better understand what users are actually looking for and surface stronger matches faster. At the same time, the company is investing heavily in safety, expanding Face Check, a facial verification system designed to reduce bots and impersonation accounts.

Closing out the presentation, Melissa Hobley, Tinder’s Chief Marketing Officer, zoomed out from the product roadmap to the brand’s cultural footprint, noting that Tinder is mentioned in billions of TikTok videos and has become shorthand for how younger generations talk about dating.

Taken together, the updates represent Tinder’s most significant evolution in years. And judging by the energy inside the El Rey this week, the company believes the next chapter of dating will be more social, more expressive and more intentional. It’s a shift being shaped right here in Los Angeles, and one that could redefine how the next generation meets.

Now onto this week’s LA venture deals, fund announcements and acquisitions.

🤝 Venture Deals

LA Companies

- Hurray’s GIRL BEER raised a $5M seed round led by Lakehouse Ventures, with participation from Spice Capital plus CPG insiders and entertainment executives, as it accelerates national expansion. The LA-based flavored light beer brand says it has already landed retail placements at Walmart, Kroger, Albertsons, and Whole Foods, and plans to use the new capital to deepen distribution, enter new markets, and ramp up marketing, alongside a rollout of seven new flavors. - learn more

- Freestyle closed a $10M Series A led by Silas Capital, with significant participation from ECP Growth. The company also noted continued backing from existing investors including Mucker Capital, Adapt Ventures, and Superangel, as it scales its premium diapers and wipes business following nationwide launches at Walmart and Target. - learn more

- MAX BioPharma announced a new investment and partnership with Technomark Life Sciences to advance Oxy210, its oxysterol-based, orally available drug candidate for MASH. Technomark is joining as a strategic lead investor by participating in MAX BioPharma’s $13M Series A to fund a Phase 1a/1b first-in-human study, and the companies say the collaboration will pair MAX’s therapeutic platform with Technomark’s drug development experience. - learn more

LA Venture Funds

- B Capital participated in ORO Labs’ $100M Series C, which was led by Brighton Park Capital and Growth Equity at Goldman Sachs Alternatives, as the company pushes deeper into what it calls agentic procurement orchestration. ORO said the new funding follows 300% revenue growth over the past year and will be used to speed up product development, expand go-to-market and customer teams globally, and broaden enterprise use cases across procurement, finance, legal, and supply chain workflows. - learn more

- Aliment Capital participated in Tropic’s oversubscribed $105M Series C, which was co-led by Forbion’s Bioeconomy Fund and Corteva as the company scales the commercial rollout of its gene-edited tropical crops. Tropic said the funding will help expand production of its banana portfolio, accelerate its banana and rice pipelines, and support entry into additional climate-resilient crops, following the 2025 launch of its first new banana varieties in more than 75 years and demand that is already outpacing supply. - learn more

- B Capital doubled down in Axiom’s $200M Series A, which valued the company at more than $1.6 billion and was led by Menlo Ventures. Axiom said the new funding will help it extend its lead from formal mathematics into what it calls “Verified AI,” with plans to apply its technology beyond mathematical discovery into software and hardware verification. - learn more

- WndrCo participated in Quince’s $500M Series E, a round led by ICONIQ that values the manufacturer-to-consumer retail platform at $10.1B post-money. Quince says it will use the fresh capital to accelerate growth and global expansion of its proprietary M2C operating system, which uses AI-driven demand forecasting and direct factory partnerships to cut traditional retail markups. Other investors in the round included Basis Set Ventures, Wellington Management, MarcyPen Capital Partners, Baillie Gifford, Notable Capital, and DST Global. - learn more

- Matter Venture Partners co-led Eridu’s oversubscribed Series A, part of $200M+ raised as the AI networking startup emerges from stealth to tackle what it calls the “network wall” bottleneck in AI data centers. - learn more

- Matter Venture Partners participated in Rhoda AI’s $450M Series A, backing the startup as it comes out of 18 months in stealth with FutureVision, a video-predictive control platform aimed at helping robots operate reliably in messy, real-world industrial environments. The round included a large syndicate of investors, including Capricorn Investment Group, Khosla Ventures, Leitmotif, Mayfield, Premji Invest, Prelude Ventures, Temasek, Xora, and John Doerr, and the company says the funding will accelerate development and industrial deployments. - learn more

- Halogen Ventures participated in Rasa Legal’s $5M late-seed round, backing the company’s push to scale its tech-enabled criminal record sealing and expungement service nationwide. The round was led by Rethink Education with participation from Social Finance and the Richard King Mellon Foundation, and Rasa says the funding will help it expand leadership, speed product development, and grow beyond its current footprint (Utah, Arizona, and Pennsylvania). - learn more

- Halogen Ventures participated in Nyad’s $1.3M oversubscribed pre-seed round, backing the Birmingham-based startup as it launches an AI decision-support tool for wastewater treatment operators. The round was led by Boost VC with participation from Draper Associates, Ollin Ventures, Apprentis, First Avenue Ventures, and strategic angel Troy Wallwork, and Nyad says it will use the funding to hire, grow customers, and keep building the product as retirements thin the wastewater workforce. - learn more

- MANTIS VC participated in Scanner’s $22M Series A, which was led by Sequoia Capital and also included CRV, as the company builds a high-speed security data layer for AI-driven threat investigation. Scanner said the funding comes as security teams at companies like Notion, Ramp, and BeyondTrust use its platform to search years of log data quickly and power agentic workflows that help hunt threats, triage alerts, and investigate incidents more efficiently. - learn more

- Chapter One participated in Zcash Open Development Lab’s $25M+ seed round, joining a syndicate that included Paradigm, a16z crypto, Winklevoss Capital, Coinbase Ventures, Cypherpunk Technologies, and Maelstrom. The new company, formed by former Electric Coin Company team members, said the funding will support continued development of privacy-focused infrastructure for the Zcash ecosystem, including its self-custodial wallet and broader shielded payments tooling. - learn more

- CIV participated in Isembard’s $50M Series A, which was led by Union Square Ventures and also included Tamarack Global, IQ Capital, and existing backer Notion Capital. Isembard said the new funding will help it open 25 AI-powered factories by the end of 2026, expand its engineering team, and enter Germany, France, and Ukraine as it scales software-driven component manufacturing for aerospace and defense customers. - learn more

- WndrCo participated in Crafting’s $5.5M seed round, which was led by Mischief as the startup launched general availability for Crafting for Agents. The company said the new capital will support its push to become core infrastructure for AI-driven engineering teams, giving agents secure access to production-like environments so they can validate, test, and ship code inside complex enterprise systems used by customers including Brex, Faire, and Webflow. - learn more

LA Exits

- Hireguide has been acquired by HireVue, which is buying Hireguide’s underlying technology and bringing the Hireguide team into HireVue’s product org. HireVue says the deal accelerates its agentic AI roadmap, starting with a voice-based AI interviewer designed to help employers qualify candidates earlier and run smarter, more conversational hiring workflows. - learn more

- Ultracor has been acquired by Applied Aerospace & Defense, bringing the California-based maker of specialized honeycomb core materials into Applied’s advanced composites platform. Applied says the deal supports its selective vertical integration strategy by strengthening supply chain control and boosting speed and capacity for space and defense programs, from satellites and missiles to antennas, radomes, and next-gen aircraft. - learn more

LA based Arc, founded in 2021 by a team of SpaceX alumni, announced a $50M Series C this week, led by Eclipse, a16z, Menlo Ventures, Lowercarbon, Necessary Ventures, and Offline Ventures, as it pushes deeper into commercial maritime. The raise follows Arc’s $160M contract with Curtin Maritime to deliver eight hybrid-electric tugboats beginning at the Port of Los Angeles, with the first expected to hit the water this year.

Imsage Source: Arc

Imsage Source: Arc

That feels notable not just because of the funding, but because it marks a clear evolution in Arc’s business. What started as a premium electric boat company is now making a serious push into the industrial side of maritime transportation, with ambitions spanning tugboats, ferries, and defense vessels.

There is also something fitting about this story happening in Los Angeles. This is a city known for spectacle, but Arc is building in a category where performance actually has to perform. No amount of branding can fake a working tugboat, and that is exactly why this moment feels worth paying attention to.

Now, onto this week’s LA venture deals, fund announcements and acquisitions.

🤝 Venture Deals

LA Companies

- Talino closed a $7.5M Series A led by Chemonics International, with participation from Mt Sinai Capital and Gulf Blvd, as it shifts from a venture studio into what it calls a global fintech foundry. The company said the new funding will help build an API-first cross-border payments infrastructure layer connecting the U.S. with emerging markets, starting with the Philippines, where it is targeting faster, more compliant financial product launches and modernizing legacy rails with stablecoin and real-time payment capabilities. - learn more

- PADO AI raised a $6M seed round led by NovaWave Capital to expand its AI-powered orchestration software for mid-market colocation data centers. The company said the funding will support product delivery and global growth as it helps operators better manage power, compute, cooling, and distributed energy resources to increase GPU utilization and maximize “compute per megawatt” without requiring major new infrastructure buildouts. - learn more

- Meadow Memorials raised a $9M Series A led by Lachy Groom and Haystack to expand its software-enabled funeral planning platform, which lets families arrange services online or by phone. Founded in 2024 by former Stripe executive Sam Gerstenzang and Emma Gilsanz, the company says it is using a real-estate-light model to offer lower-cost funerals as it expands beyond California into states including Texas, Washington, and Arizona. - learn more

LA Venture Funds

- Anthos Capital participated in Bluesky’s $100M Series B, which was led by Bain Capital Crypto and also included Alumni Ventures, Bloomberg Beta, Knight Foundation, and True Ventures. The company said the round gave it the resources to scale both the Bluesky app and the broader AT Protocol ecosystem, which it says has grown to more than 43 million users and now supports a fast-expanding network of third-party apps and developers. - learn more

- Navigate Ventures participated in VerbaFlo’s oversubscribed $7M seed round, which was led by Pi Labs and also included Haatch and Old College Capital. VerbaFlo said it plans to use the funding to scale its conversational AI platform for real estate operators, building on traction across more than 200,000 units and expanding further into markets including the U.S., Middle East, and Australia. - learn more

- March Capital participated in Xage Security’s $15M equity financing round, which was led by Piva Capital as the company posted 81% year-over-year revenue growth and expanded its Zero Trust platform for AI and critical infrastructure. Xage said the funding, which closed in December 2025, will support go-to-market expansion and continued product innovation, including new AI security capabilities, as demand grows across sectors such as energy, manufacturing, utilities, transportation, and defense. - learn more

- B Capital led Knox Systems’ $25M Series A, backing the company’s push to scale what it says is the largest AI-managed federal cloud and dramatically shorten the FedRAMP authorization process for software vendors. Knox said the new funding will help accelerate growth after its June 2025 seed round, with the goal of helping customers achieve FedRAMP authorization in as little as 90 days at roughly 90% lower first-year cost, while expanding adoption across both government and commercial environments. - learn more

- WndrCo participated in Tenkara’s $7M round, which was led by True Ventures as the company builds AI-powered operations agents for American manufacturers. Tenkara said it is creating tooling to help factories handle sourcing and operational work more efficiently at a time of rising supply-chain pressure, with backing from a broader investor group that also included Articulate Capital, Night Capital, HF0, SF1, and Transpose Platform. - learn more

- Aurora Capital participated in Niv-AI’s $12M seed round, backing the startup alongside Glilot Capital, Grove Ventures, Arc VC, Encoded VC, and Leap Forward as it emerged from stealth. Niv-AI is building sensors and software to measure millisecond-scale GPU power surges and help data centers use electricity more efficiently, with plans to deploy its system in a handful of U.S. facilities within the next six to eight months. - learn more

- Clocktower Technology Ventures participated in Fuse’s $25M Series A, which TechCrunch reported was led by Footwork, Primary Venture Partners, NextView Ventures, and Commerce Ventures, with Fuse also naming Clocktower Ventures among its backers. The company said it plans to use the funding to expand its AI-native loan origination and account opening platform for credit unions, building on traction with more than 100 customers and a $5M “rescue fund” aimed at helping institutions switch off legacy systems. - learn more

- Kairos Ventures participated in Alomana’s €4M seed round, which was led by CDP Venture Capital and also included Founders Factory, Italian Angels for Growth, Club degli Investitori, and others. Alomana said it will use the funding to strengthen its enterprise AI platform, add more capabilities for autonomous workflow automation, and support larger deployments across Europe as demand grows in sectors like finance, manufacturing, and pharma. - learn more

LA Exits

- Optimal’s Entertainment Media division is being acquired by Capstone Point Holdings, with the business set to operate under its legacy name, Optimad Media, following the deal. The transaction keeps founder Kevin Weisberg in place to lead the company from Los Angeles, while giving Optimad more backing to expand its entertainment media planning, buying, and prints-and-advertising investment capabilities across theatrical, streaming, and broadcast campaigns. - learn more