Shutterstock

Venture Deals in LA Are Slowing Down, And Other Takeaways From Our Quarterly VC Survey

It looks like venture deals are stagnating in Los Angeles.

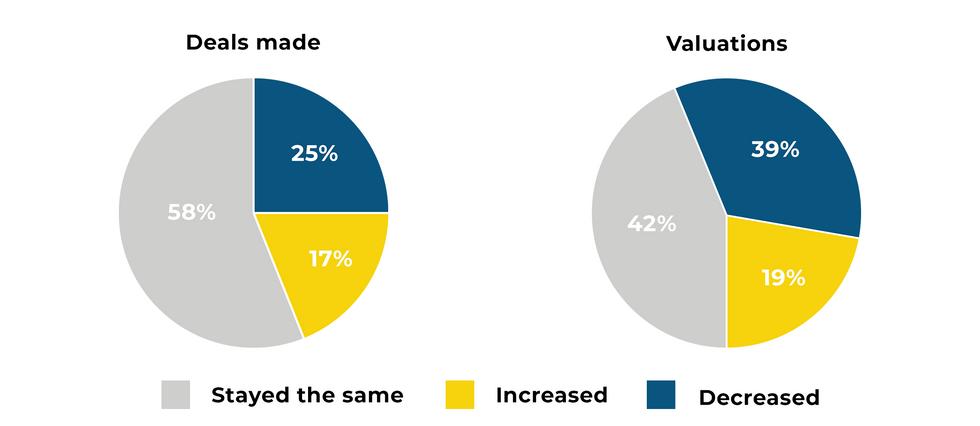

That’s according to dot.LA’s most recent quarterly VC sentiment survey, in which we asked L.A.-based venture capitalists for their take on the current state of the market. This time, roughly 83% of respondents reported that the number of deals they made in L.A. either stayed the same or declined in the first quarter of 2022 (58% said they stayed the same compared to the fourth quarter of 2021, while 25% said they decreased).

That’s not hugely surprising given the sluggish dynamics gripping the venture capital world at large these days, due to macroeconomic factors including the ongoing stock market correction, inflation and Russia’s invasion of Ukraine. While startups and VC investors haven’t been hit as hard as public companies, it looks like the ripple effects are beginning to bleed into the private capital markets.

Image courtesy of Hagan Blount

Image courtesy of Hagan Blount

In addition to slowing deal volumes, most investors said they’re seeing startup valuations lose momentum, as well: Roughly 81% said valuations either stayed the same or decreased from the previous quarter, with nearly 39% noting a decline.

Should that sentiment continue moving forward, it could spell bad news for startups as far as raising the money they need for growth, investors said.

“If I was a startup right now, I would be making sure I have plenty of runway,” said Krisztina ‘Z’ Holly, a venture partner at Good Growth Capital. “When it looks like there's some potential challenges ahead in the market, it’s good to fill your war chest.”

Among VC respondents, about 86% said they believed that valuations in the first quarter were too high—one potential reason why deals slowed down in the first quarter, according to TenOneTen Ventures partner Minnie Ingersoll. She noted that L.A.’s growing startup scene features more early-stage ventures, whose valuations haven’t come down the way later-stage startup valuations have.

“I would say we are just more cautious about taking meetings where the valuations are at pre-correction levels,” Ingersoll said. “We didn’t take meetings because their valuations weren’t in line with where we thought the market was.”

While most respondents said the Russia-Ukraine war didn’t have much impact on their investment strategies, some 22% said it did have an effect—with one VC noting they had to pass on a deal in Russia that they liked.

Is There a Flight Out of Los Angeles?

Los Angeles was heralded as the third-largest startup ecosystem in the U.S. at the beginning of the year, behind only San Francisco and New York. Yet nearly one-third (31%) of VC respondents said that at least one of their portfolio companies had left L.A. within the past year. It won’t come as a huge surprise that the city of Austin, Texas has been one of the prime beneficiaries of this shift—with roughly half of those who reported that a portfolio company had left L.A. identifying Austin as the destination.

The tech industry’s much-hyped “exodus” from California has been widely reported on, especially as more companies have embraced the work-from-home lifestyle and also opted to move their operations to lower-cost cities and states. Most notably, Elon Musk has recently moved two of his companies, electric automaker Tesla and tunnel infrastructure startup The Boring Company, from California to Texas (with both of those firms moving in and around Austin).

“In today's competitive market with lots of capital to invest, we think the next generation of successful VCs are going to be diverse in markets (not just Silicon Valley)... [and] have access to undiscovered founders from everywhere,” said one survey respondent.

NFTs Aren’t Popular With VCs—But Web 3 Is

“It’s the future,” according to one respondent. “Buckle up and get on board.”

Are NFTs...

More than 71% of VC survey respondents said they were bullish on Web3—the new blockchain-enabled iteration of the internet, which promises decentralization and a whole range of applications involving cryptocurrencies, NFTs, DeFi and more. It’s the same sentiment informing Santa Monica-based VC firm M13’s new $400 million fund, which considers Web3 a core piece of its investment thesis.

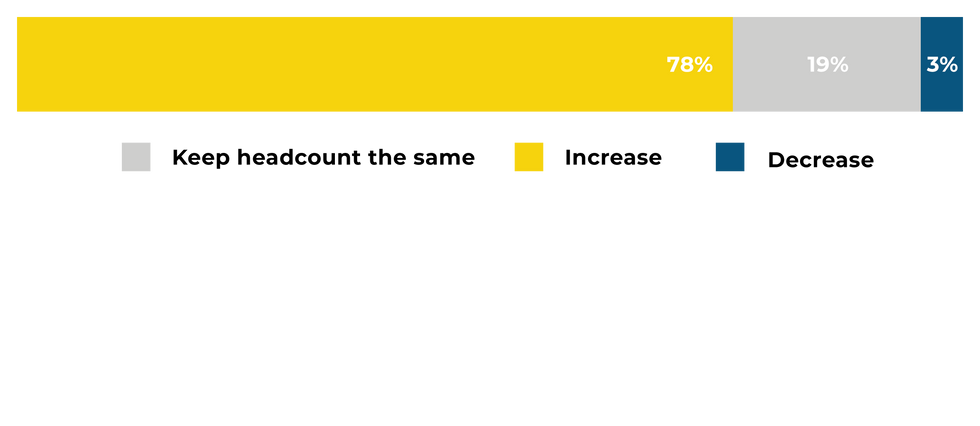

In Q2 2022, do you expect your portfolio companies to:

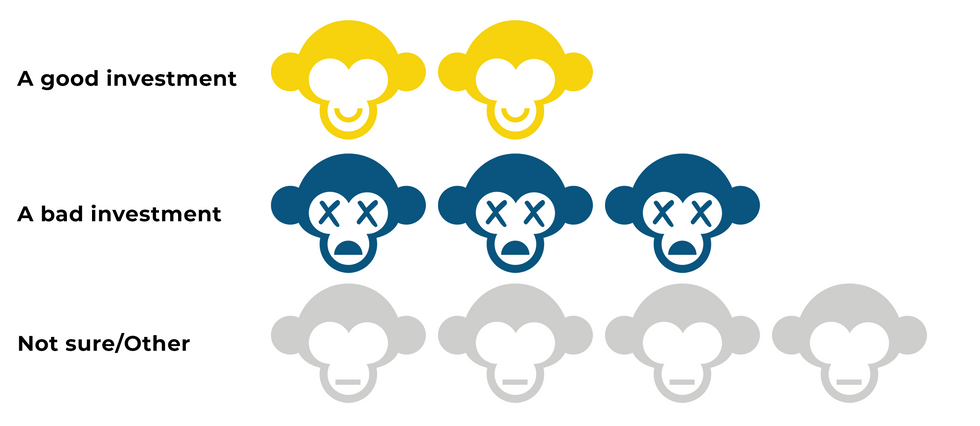

L.A. is home to an ever-growing cadre of Web3-focused startups operating across the realms of finance, entertainment and other industries. But while local investors are willing to pour money into blockchain-related ventures, one segment of the space continues to evoke skepticism: Only 18% of respondents would describe NFTs as “a good investment,” while 33% thought they were “bad” investments and 39% said they were unsure.

As in our last survey several months ago, it appears that NFTs continue to divide opinion, with respondents expressing differing perspectives on their value and utility. One referred to them as “get rich quick schemes,” but added that the art pieces and social communities that emerge from them may be valuable. Another said that “NFTs as a digital medium are a legitimate thing”—but noted the vast majority are “awful investments with no intrinsic value.”

Graphics courtesy of Hagan Blount.

From Your Site Articles

- Los Angeles Venture Funds Grow, but Spend Less in LA - dot.LA ›

- LA's Top Venture Capitalists of 2022 - dot.LA ›

- Los Angeles Venture Capital News - dot.LA ›

- Here Are Los Angeles' Top Venture Capitalists - dot.LA ›

- Venture Deals Fall in LA Amid Economic Worries - dot.LA ›

Related Articles Around the Web